In-kind vs. lump-sum funeral insurance: which suits you?

A quarter of policyholders don't even know what type of funeral insurance they have. Meanwhile, costs are rising faster than ever. In this article, we compare natura insurance and capital insurance on freedom of choice, costs and risks, so you can make a conscious decision yourself.

Imagine: you once took out a funeral insurance policy, but you actually have no idea what type it is. You're not the only one. Research by Nibud shows that a quarter of policyholders don't know what kind of funeral insurance they have. Let alone whether that insurance still provides sufficient coverage.

Meanwhile, funeral costs are rising faster than most people realize. The NOS reported in 2025 that the costs of burials and cremations had risen by about 40% over ten years. And according to CBS figures, inflation specifically for funeral services in 2025 was as high as 3.1%.

The choice between a natura insurance and a capital insurance (also called a money insurance) is therefore more relevant than ever. In this article, I'll explain the difference, without difficult jargon or sales pitches. So you can decide for yourself which type best suits your situation.

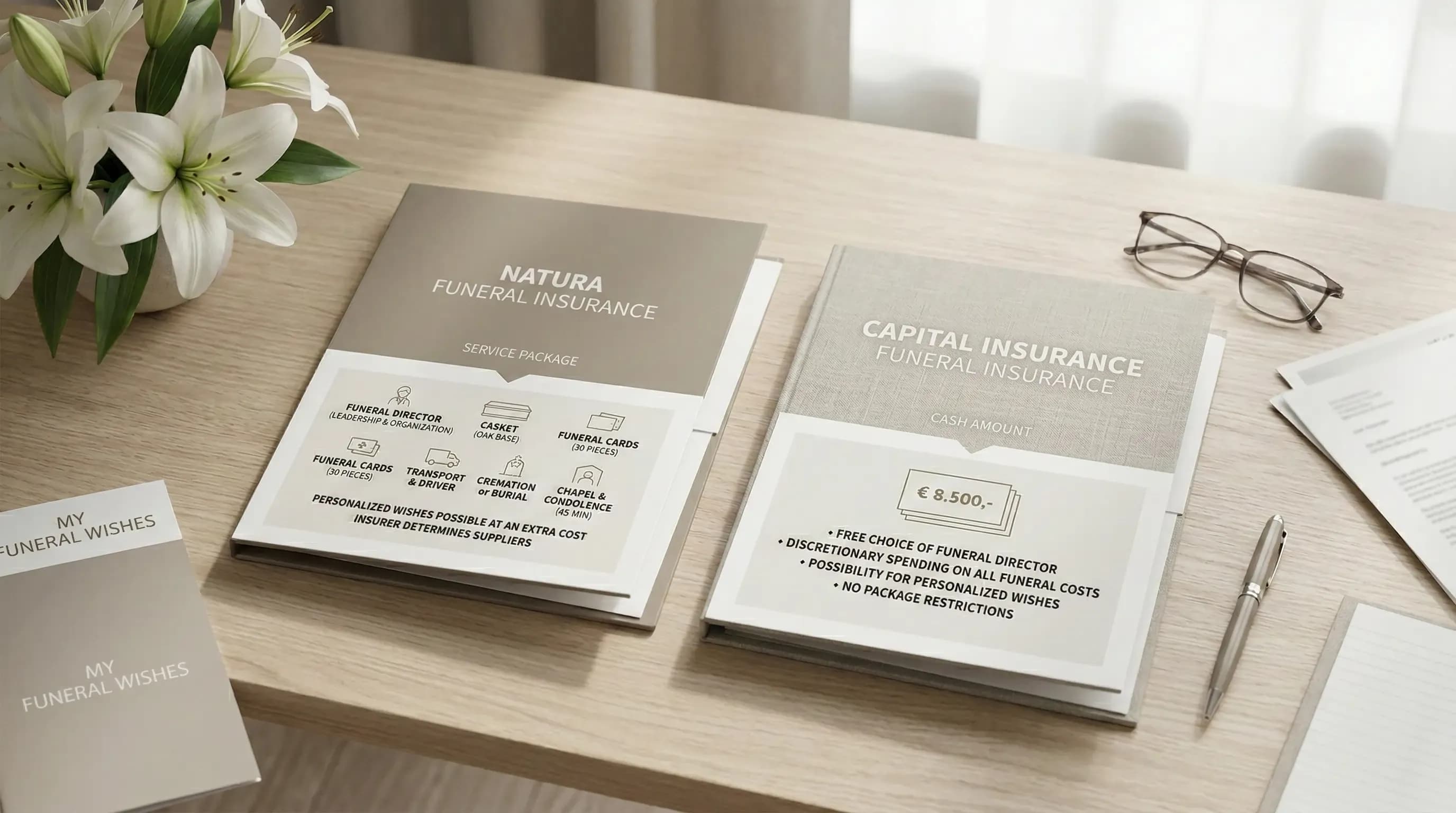

What exactly is a natura insurance?

With a natura insurance, you don't insure a sum of money, but services. Think of the final care of the deceased, funeral transport, a coffin and guidance from a funeral director. The insurer arranges the funeral itself, or has it done by an affiliated funeral company.

The big advantage: your next of kin don't have to search for a funeral director or compare prices at a moment when that's the last thing on their mind. The insurer takes that off their hands. Moreover, the value of a natura insurance in principle grows along with the rising costs of funeral services, which reduces the risk of underinsurance.

There is a downside though. With most natura policies, you're tied to the funeral director of the insurer. If you choose a different party anyway? Then your next of kin often receive only a limited reimbursement. At DELA, that reimbursement in 2026 amounts to a minimum of €3,957 (made up of €3,157 for services and a minimum of €800 as a supplementary cash amount), while the service package at DELA itself is worth an average of about €8,000, as DELA states on their website.

Practical tip: Already have a natura insurance? Check your policy conditions to see exactly what happens if your next of kin choose a different funeral director. The difference between full coverage and the limited reimbursement can be thousands of euros.

What is a capital insurance (money insurance)?

With a capital insurance, you determine in advance a fixed sum of money for which you want to be insured. When you pass away, the insurer pays out this amount to your next of kin. They may spend it at their own discretion, including on things that have nothing to do with the funeral.

That sounds attractive, but there's an important caveat. With a money insurance, the risk of underinsurance is higher. Say you take out a policy today for €9,500. In twenty or thirty years, an average funeral could easily cost double if prices keep rising as they are now. Without proper indexation (automatically letting your insured amount grow along) your policy could fall seriously short.

On top of that, a capital insurance has tax implications. The surrender value of a money insurance falls under wealth tax in box 3. In 2026, there's an exemption for the first €8,904, as confirmed by the Tax Authority. Is the value of your policy/policies above that? Then you pay tax on the excess.

Insurers such as a.s.r. and DELA both offer capital insurances with different indexation options. At a.s.r., for example, you can choose an annual increase based on the consumer price index (CPI) from CBS, or a fixed percentage of 2 to 5%.

Practical tip: Going for a capital insurance? Always check whether there's an indexation clause in your policy and whether it's activated. Without indexation, you run a real risk of underinsurance.

The real costs in 2026: what are we actually talking about?

To make a good choice between natura and capital, it helps to know what a funeral actually costs in 2026.

Monuta states on their website that next of kin in the Netherlands spend on average between €7,000 and €11,500 on a funeral. Nibud mentioned an average of €7,500 in their research, but that figure dates from 2017 and is quite outdated given the inflation of recent years.

And then there's this: nearly four in ten Dutch people underestimate the costs of a funeral. Research shows that 38.2% thinks a funeral costs less than €7,500. Especially young people between 18 and 34 often have no realistic picture and moreover haven't arranged anything.

Practical tip: Use the online funeral cost calculators from insurers to make a personal estimate. Fill in your own preferences (cremation or burial, number of guests, with or without a coffee gathering) and you'll get a more realistic picture than the national averages.

Underinsurance: the silent risk with both types

Underinsurance is perhaps the biggest risk you need to account for, regardless of which type of insurance you choose. Combined figures from CBS and the NOS show that about 40% of all policyholders in the Netherlands are underinsured. With a total of about five million policyholders, that means roughly two million people who are insured for less than an average funeral costs.

With a capital insurance, underinsurance mainly occurs because the insured amount lags behind the rising funeral costs. Many older policies are still set at amounts of €3,000 to €4,000, while the actual costs are now double or more.

With a natura insurance, the risk of underinsurance is smaller, because the insured services grow in value along with the market. But a problem can also arise here if your wishes change. Perhaps in ten years you'll want a more elaborate ceremony, a special venue or sustainable alternatives such as a natural burial. Those extras often fall outside the standard service package.

Incidentally, a third variant, the combination insurance, offers a middle ground. With this, you get a basic package of services (natura) supplemented with a freely spendable cash amount for extra wishes. Insurers such as DELA and Monuta offer this type.

Practical tip: Ask your insurer for a current overview of your coverage and compare it with the current average funeral costs. Do this at least once every five years. Need to top up your insurance? That can be done easily online with most insurers.

Freedom of choice versus peace of mind: what matters more?

The fundamental difference between natura and capital comes down to a personal consideration: do you want your next of kin to be relieved of as much as possible, or would you rather give them maximum freedom of choice?

With a natura insurance, peace of mind takes center stage. The insurer or an affiliated funeral director takes most of the work off their hands. That's welcome during a period when your next of kin are probably occupied with entirely different things than comparing quotes. The premium for a natura insurance is also often slightly lower than for a capital insurance with comparable coverage. On the other hand, you're tied to the insurer's service provider.

With a capital insurance (money insurance), freedom takes center stage. Your next of kin choose which funeral director to engage and how to spend the money. That works well if you already have a preference for a specific local funeral director, or if you want to be buried abroad. a.s.r. exclusively offers capital insurances: the entire organization falls to the next of kin, but they also have full control.

The Authority for the Financial Markets (AFM) emphasizes that insurers are obligated to clearly inform about costs, coverage and risks. This applies to both types of insurance. Are you being approached by an advisor? Then they are required to disclose advisory fees (on average €350 to €500) in advance. When in doubt: always check whether the advisor has an AFM registration.

Practical tip: Consider whether your next of kin are the type who like to take control themselves, or whether they'd prefer to have to arrange as little as possible. This often says more about the right choice than the premium.

Natura, capital or combination: the choice in practice

Let's make it concrete. Below is an overview of when which type tends to be the best fit in practice.

A natura insurance often fits well if you want your next of kin to have to arrange as little as possible, you have no strong preference for a specific funeral director, you want to pay a slightly lower premium and you like the idea that your insured value automatically grows along with the costs.

A capital insurance often fits better if maximum freedom of choice is important to you, you already know which funeral director you want to go to, you want to be buried or cremated abroad, or if your next of kin want to be able to freely spend the remaining amount.

A combination insurance is worth considering if you want the best of both worlds: a basic package of services for the core of the funeral, supplemented with a freely spendable amount for personal wishes such as flowers, a coffee gathering or a special venue.

At DELA, the FuneralPlan in services (natura) consists of a service package supplemented with a cash amount of at least €800. At Monuta, you can choose a combination insurance with an insured amount of €9,500 where a funeral director arranges the core. And at a.s.r., it's exclusively a capital insurance where everything is freely spendable.

Conclusion: make a conscious choice (and check your policy)

There is no universally "best" type of funeral insurance. The right choice depends on what you find important: peace of mind or freedom, certainty or flexibility. What does apply universally: regularly check whether your policy still matches reality. With funeral costs averaging between €7,000 and €12,000 in 2026 and rising significantly each year, an outdated policy is a bigger risk than many people think.

This article is intended to inform you, not to provide personal financial advice. If in doubt about your situation, it's always wise to contact an independent financial advisor with an AFM registration.

Want to see which funeral insurance best suits your wishes? Compare funeral insurances on Eindstation.nl and discover in a few steps which type and coverage match your situation.