In-kind vs. lump-sum funeral insurance: which suits you?

Anyone who wants to take out funeral insurance quickly faces an important decision: do you choose an in-kind insurance policy or a lump-sum insurance policy? Both forms offer financial security for loved ones, but differ significantly in flexibility, payout structure, and premium build-up.

The right choice depends on your personal wishes, financial situation, and the level of control you want to maintain over your funeral. In this article, you will discover the key differences between in-kind vs. lump-sum insurance, including advantages and disadvantages, so you can determine what suits you best.

What is an in-kind insurance policy?

How does an in-kind policy work?

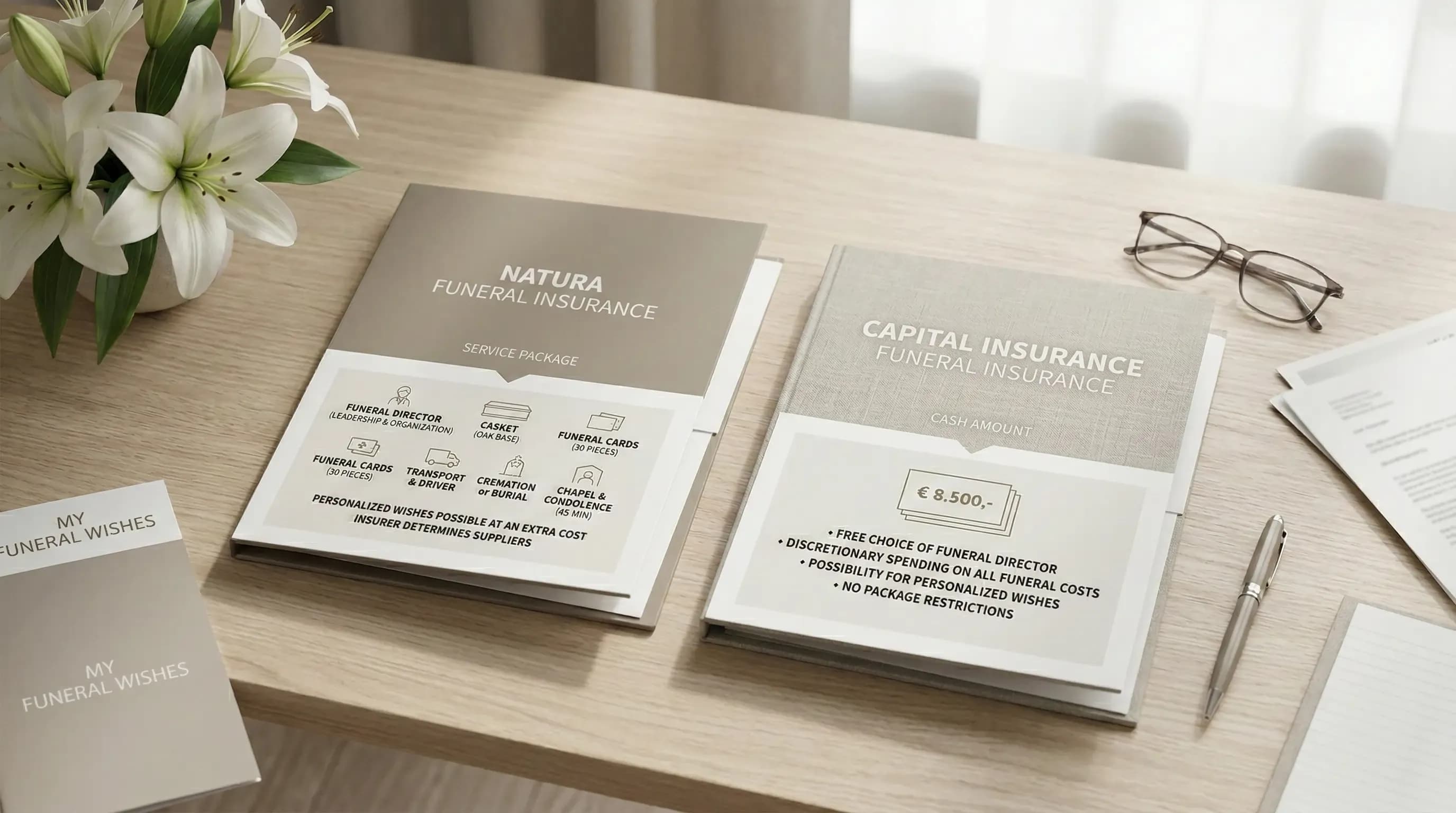

With an in-kind insurance policy, funeral-related services are arranged and paid for directly by the insurer. This includes:

- The funeral director

- A coffin or urn

- Laying out and transportation

- Use of a chapel

- Administrative handling

Loved ones do not receive a sum of money, but a package of services.

Advantages of an in-kind insurance policy

- Less administrative burden for loved ones

- Clarity about what has been arranged

- Protection against rising funeral costs (with full coverage)

For people who value being fully taken care of, this is often an attractive option.

Disadvantages of an in-kind insurance policy

- Less freedom in choosing a funeral provider

- Limited flexibility for personal wishes

- Possible additional payments for alternative choices

What is a lump-sum insurance policy?

How does a lump-sum insurance policy work?

With a lump-sum insurance policy, loved ones receive a predetermined amount of money. They can freely spend this amount on the funeral.

The payout can be used for:

- Burial or cremation

- Ceremony and catering

- Grave costs or urn

- Personal wishes

Advantages of a lump-sum insurance policy

- Full freedom of choice

- Flexibility in spending

- Suitable for personal or unique funerals

Disadvantages of a lump-sum insurance policy

- Loved ones must arrange more themselves

- Risk that the amount is insufficient due to inflation

- No fixed price agreements with funeral providers

Key differences between in-kind and lump-sum

Flexibility

A lump-sum insurance policy offers more freedom. An in-kind insurance policy provides more structure and certainty.

Costs and premium

For both types, the premium depends on age, duration, and insured value. An in-kind policy may appear more affordable due to fixed agreements with partners, while a lump-sum insurance policy is more sensitive to inflation if there is no indexation.

Administrative burden for loved ones

Do you want to relieve your loved ones as much as possible? Then in-kind is often more practical. Do you want maximum freedom of choice? Then lump-sum fits better.

When do you choose which funeral insurance?

An in-kind insurance policy suits you if:

- You find certainty more important than flexibility

- You want to burden your loved ones as little as possible

- You are satisfied with a standard package

A lump-sum insurance policy suits you if:

- You have specific wishes for your funeral

- You want complete freedom of choice

- You want your loved ones to make their own decisions

Is a combination insurance policy an alternative?

Some insurers offer a combination of in-kind and lump-sum insurance. In this case, part is provided in services and part is paid out as a cash amount. This can be a good middle ground for those who want both certainty and flexibility.

Conclusion

The choice between in-kind vs. lump-sum insurance fully depends on your personal preferences. Do you want maximum peace of mind and fixed agreements? Then an in-kind insurance policy is suitable. Do you value freedom and customization more? Then a lump-sum insurance policy is a better fit.

Take the time to compare premiums, conditions, and flexibility. This way, you choose funeral insurance that truly matches your wishes and prevent financial surprises for your loved ones.